Most people start investing before they start protecting.

They open SIPs.

They buy stocks.

They plan retirement.

But one unexpected expense can break everything.

Job loss.

Medical emergency.

Family responsibility.

Sudden relocation.

That is where an emergency fund becomes your financial shock absorber.

💡 What Is an Emergency Fund?

An emergency fund is money kept aside only for unexpected situations — not vacations, gadgets, or festivals.

It gives you three powerful benefits:

• Peace of mind

• Protection from debt

• Ability to continue long-term investments without interruption

Without it, one crisis forces you to:

• Break investments

• Swipe credit cards

• Take personal loans at high interest

🧠 Why 6 Months Expense Model Works

The simplest rule used globally is:

👉 Save at least 6 months of essential expenses

This covers the average time required to:

• Find a new job

• Recover from a health situation

• Stabilize finances after disruption

If your job is unstable, business income fluctuates, or you have dependents, the buffer should be higher (9–12 months).

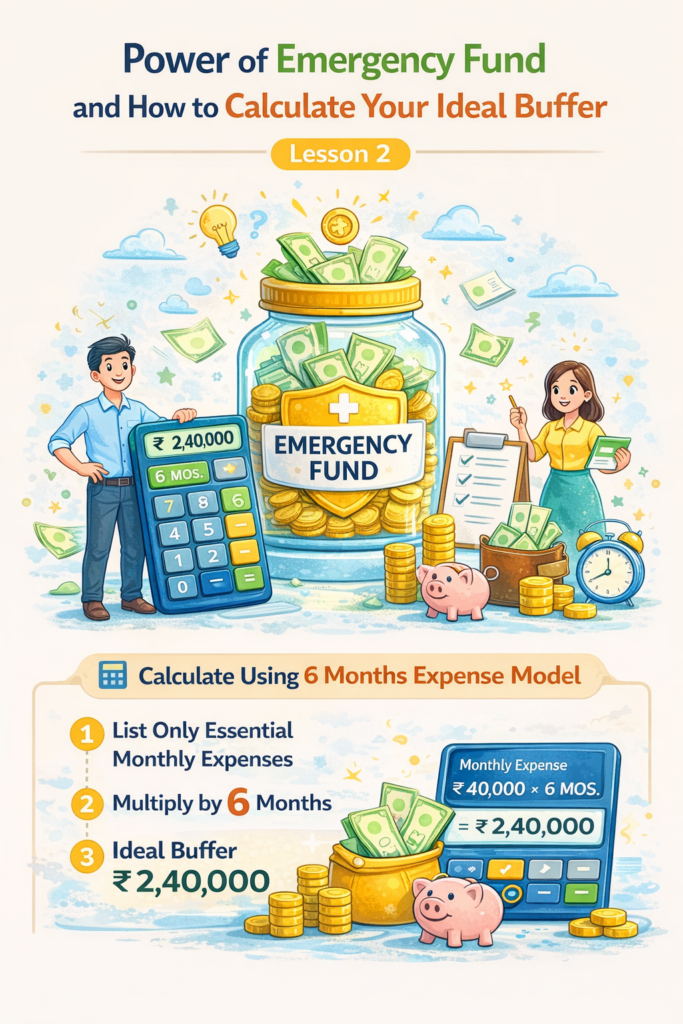

📊 Step-by-Step : How to Calculate Your Ideal Emergency Fund

Step 1 : List Only Essential Monthly Expenses

Include:

• Rent / EMI

• Groceries

• Utilities

• Insurance premiums

• School fees

• Basic transport

• Medicines

Exclude:

• Shopping

• Travel

• Dining out

• Entertainment

Step 2 : Calculate Monthly Essential Expense

Example:

Rent / EMI → ₹20,000

Groceries → ₹10,000

Utilities → ₹4,000

Insurance → ₹3,000

Transport → ₹3,000

Total essential expense = ₹40,000

Step 3 : Apply the 6 Month Formula

Emergency Fund = Monthly Essential Expense × 6

₹40,000 × 6 = ₹2,40,000

That is your minimum safety buffer.

🔁 When Should You Increase the Buffer?

Increase to 9–12 months if:

• Single income family

• Freelance or business income

• Medical history in family

• Planning career break

• High EMIs

🏦 Where Should You Keep Emergency Fund?

Emergency fund should be safe and liquid — not invested for returns.

Good options:

• Savings account

• Sweep FD

• Liquid mutual funds

Avoid:

• Stocks

• Long lock-in investments

• Real estate

Because emergency money must be available immediately.

⚠️ Biggest Mistake People Make

They invest first and plan safety later.

Then one emergency forces them to exit investments at the worst time.

Emergency fund is not low priority money.

It is the foundation of wealth building.

✅ Simple Action Plan

Calculate essential expenses

Multiply by 6

Start building monthly

Automate savings

Review every year

Even small monthly contributions build strong protection.

🔎 How MoneyNivesh Tools Can Help

You can use the MoneyNivesh Goal Planning Calculator to:

• Estimate monthly expenses

• Adjust inflation impact

• Set emergency fund targets

• Track progress alongside investments

Because wealth building starts with stability, not risk.

Your emergency fund is your first financial freedom milestone.