School taught us many useful things:

- Algebra

- History

- Discipline

But when it came to money, school taught us almost nothing.

Worse, it taught us half-truths and dangerous simplifications that silently cost most Indians lakhs of rupees over a lifetime. Let us talk about the five biggest financial lies we were taught growing up and what the truth actually is.

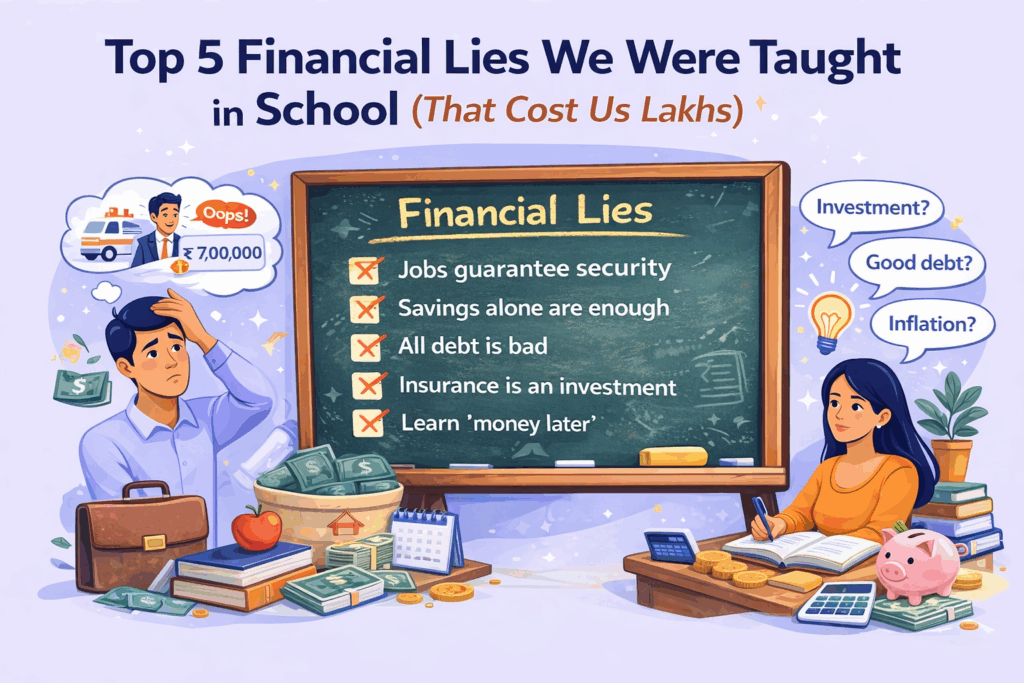

Lie 1: Study Hard, Get a Job, and You Will Be Financially Secure

This is the most expensive lie of all.

Yes, education matters.

Yes, jobs are important.

But a job alone does not guarantee financial security.

What school did not teach us:

- Salaries stop when you stop working

- Inflation reduces purchasing power every year

- Medical emergencies do not respect job titles

Millions of educated and well-paid people:

- Live paycheck to paycheck

- Have no emergency fund

- Depend on loans during crises

Income is not wealth. Financial systems are.

Lie 2: Saving Money Is Enough

We were taught to save money for the future.

Nobody explained where or how.

So we saved in savings accounts, fixed deposits, and cash.

Meanwhile, inflation quietly did its work.

The uncomfortable truth is simple.

If your money grows at 4 to 5 percent and inflation is 6 to 7 percent, you are losing money every year.

Saving without investing is not safety.

It is slow financial decay.

Lie 3: Debt Is Always Bad

School drilled this idea into us repeatedly.

Loans are dangerous. Avoid debt.

This created fear, not understanding.

The reality is that there are two types of debt.

- Bad debt such as credit cards, lifestyle EMIs, and consumption loans

- Productive debt such as education loans or reasonable home loans

Because this difference was never explained, many people either avoid useful leverage or misuse expensive debt blindly.

Debt is a tool. Ignorance is the danger.

Lie 4: Insurance Is an Investment

This lie destroyed wealth for an entire generation.

Many Indians were told to buy insurance because it gives returns.

So they bought endowment plans, money-back policies, and complex products they never understood.

What actually happened:

- Low insurance cover

- Poor returns

- Long lock-in periods

- Missed wealth creation

Insurance is for protection.

Investment is for growth.

Mixing the two is one of the costliest financial mistakes.

Lie 5: You Will Figure Money Out Later

This lie is subtle but dangerous.

We were told to focus on studies first and worry about money later.

But money decisions begin early.

- First salary

- First loan

- First credit card

- First insurance policy

Mistakes made in your twenties quietly compound into delayed investing, poor risk management, and financial anxiety in your forties.

Money ignored early becomes money problems later.

Why These Lies Cost Us Lakhs

Money compounds over time.

So do mistakes.

A delayed SIP can cost lakhs.

Wrong insurance choices can wipe out savings.

Ignoring inflation destroys purchasing power.

Bad debt traps future income.

None of this is taught formally.

Most people learn it the hard way.

What Should Have Been Taught Instead

If schools taught just these basics, financial stress would reduce dramatically:

- How money grows over time

- The difference between income and wealth

- Basics of investing and inflation

- Insurance as protection, not investment

- The importance of early financial discipline

Final Thought

You were not taught about money.

That is not your fault.

But once you know better, ignoring it becomes a choice.

Financial literacy is not about becoming rich overnight.

It is about not staying confused for decades.

MoneyNivesh Takeaway

- School taught us how to earn marks.

- MoneyNivesh exists to help you protect and grow money with clarity.

.