You buy health insurance thinking, “At least hospital bills are covered.”

But after hospitalization, you still pay ₹1–3 lakhs from your pocket.

No fraud.

No rejection.

Just one hidden clause quietly destroying your claim:

👉 Room Rent Limit Clause

Let’s decode why this clause is one of the biggest money traps in Indian health insurance.

🏥 What Is the Room Rent Limit Clause?

The Room Rent Limit is the maximum amount per day your insurance company will pay for your hospital room.

It’s usually defined as:

1% of Sum Insured per day, or

A fixed cap (₹3,000 / ₹5,000 / ₹10,000 per day)

If you choose a room that costs more than the allowed limit, the insurer doesn’t just reduce the room rent…

👉 They proportionately reduce the entire hospital bill.

That’s where the real damage happens.

💣 Why Is It Called a “Silent Hospital Bill Killer”?

Because:

Your claim is not rejected

The policy is active

The treatment is covered

Yet, you still lose a huge portion of your claim.

Most policyholders only discover this clause after discharge, when the final bill arrives.

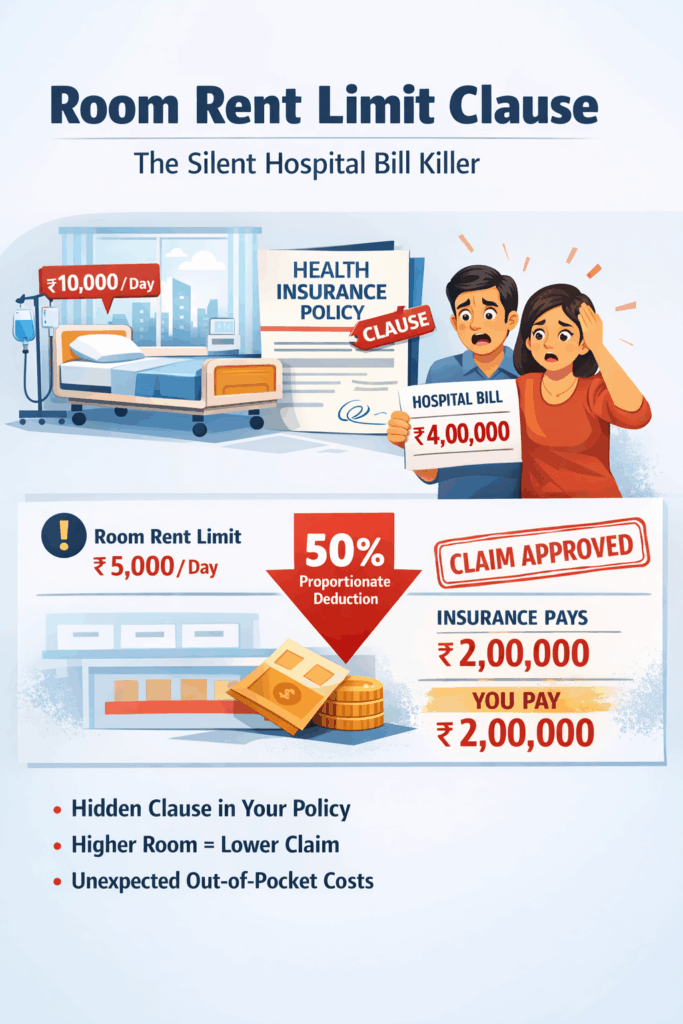

📊 Real-Life Example (Very Common Case)

Policy Details

Sum Insured: ₹5,00,000

Room Rent Limit: 1% = ₹5,000 per day

Hospital Choice

Private room cost: ₹10,000 per day

Hospital stay: 5 days

Total Hospital Bill

Room charges: ₹50,000

Other charges (doctor, surgery, ICU, medicines): ₹3,50,000

Total bill: ₹4,00,000

❌ What Insurer Does

Room chosen is double the allowed limit.

So insurer applies proportionate deduction:

Allowed room rent = ₹5,000

Actual room rent = ₹10,000

Ratio = 50%

👉 Entire bill is reduced by 50%

Final payout by insurer: ₹2,00,000

Out-of-pocket expense for you: ₹2,00,000 😨

⚠️ Why Other Charges Also Get Cut?

Because many hospital costs are linked to room category:

Doctor consultation fees

Surgeon charges

Nursing charges

OT & procedure costs

Higher room = higher overall tariff.

Insurers argue:

“You voluntarily chose a higher-cost ecosystem.”

And legally, they’re right—if the clause exists in your policy.

🚩 Why Most Indians Fall Into This Trap

Agents focus on low premium, not clauses

Buyers ignore policy wordings

Hospitals upgrade rooms automatically during admission

Patients assume “room doesn’t matter much”

Employer policies hide limits in fine print

Result? Financial shock during medical emergencies.

✅ How to Protect Yourself (Very Important)

1️⃣ Buy Policies with “No Room Rent Limit”

This is the safest option.

Most good modern policies offer:

Any room (except suites)

No proportionate deduction

2️⃣ If Limit Exists, Choose Room Carefully

Always confirm:

Allowed room rent before admission

Ask hospital billing desk to stick to eligibility

3️⃣ Avoid %-Based Room Rent Limits

Prefer:

“Single private AC room allowed”

Instead of:“1% of sum insured”

4️⃣ Be Extra Careful with Corporate Insurance

Many employer policies still have:

₹3,000–₹5,000 room caps

Hidden proportionate clauses

Always ask HR for policy T&C.

🧠 Key Takeaway

Room rent is not just about comfort.

It decides how much your insurer will actually pay.

A cheap policy with room rent limits can cost you lakhs during hospitalization.

Before buying or renewing health insurance, ask one simple question:

👉 “Is there any room rent limit or proportionate deduction clause?”

If the answer isn’t crystal clear, walk away.

📌 Final Thought

Health insurance is meant to reduce stress, not add financial anxiety.

Understanding clauses like Room Rent Limit separates:

Smart buyers ❌ from regretful buyers

Protection ✅ from false security

Disclaimer: Policy terms may vary across insurers. Always read policy wording before purchase.