A real-life reminder that corporate health insurance is not complete protection

Amit was confident.

After all, he worked in a reputed IT company in NCR.

A decent salary.

A rented 2BHK in Noida.

And the comfort of knowing that his company provided ₹5 lakh corporate health insurance for his family.

“Why waste money on a separate health insurance policy?”

That’s what he told his friends back in Kolkata.

Like many corporate employees in India, Amit believed one thing:

Corporate health insurance is enough.

He was wrong.

The Comfortable Illusion

Amit moved from Bengal to NCR eight years ago.

Life slowly fell into place:

Monthly EMIs and rent

Weekend grocery runs

Occasional family trips

SIPs that he paused and resumed

And savings he felt proud of

His mother lived with them now, growing older, diabetic, yet medically stable.

No red flags.

No hospital visits.

No reason to worry.

Or so it seemed.

Then Came One Phone Call

One evening, his wife called him at work.

“Your mother fainted. We’re going to the nearest hospital.”

By the time Amit reached, the doctors had already shifted her to ICU.

Diagnosis:

Severe infection

Complications due to diabetes

Immediate monitoring required

The doctor spoke calmly.

“She’ll need ICU care for at least 5–6 days.”

Amit nodded, trying to stay composed.

Then came the line that changed everything:

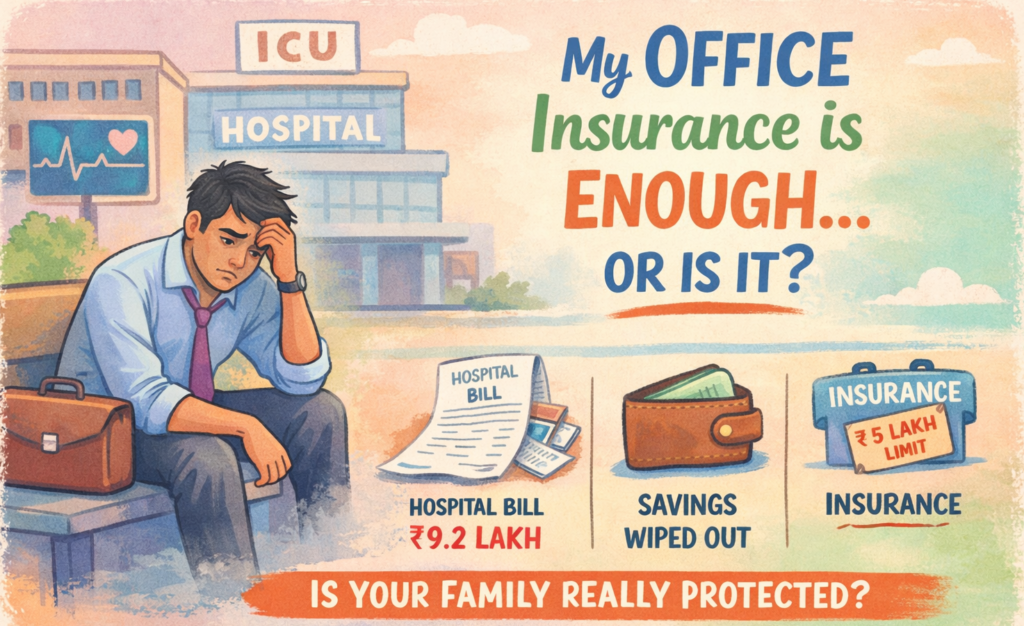

“Estimated cost will be around ₹8–10 lakhs.”

“We Have Insurance”

Amit felt relieved.

He informed the hospital desk:

“We have corporate health insurance. Cashless.”

The executive smiled politely.

“Sir, your policy covers ₹5 lakhs.

ICU room rent has a sub-limit.

Some medicines and consumables are not covered.”

Amit didn’t understand half of it.

He just heard one thing:

You will have to pay the rest.

Five Years. One Bill. Zero Savings.

In the last five years:

ICU charges had doubled

Medicine costs had shot up

Diagnostic tests were no longer cheap

Even “basic” hospital rooms cost more than monthly rent

The final bill came to ₹9.2 lakhs.

Insurance paid:

₹4.7 lakhs (after deductions)

Amit paid:

His emergency fund

His fixed deposits

His wife’s gold savings

A personal loan

Years of disciplined saving…

Gone in one medical emergency.

The Question That Haunted Him

That night, sitting outside the ICU, Amit kept thinking:

“What if my company changes?”

“What if I lose my job?”

“What if this happens again?”

He remembered rejecting a ₹20,000 annual premium for a personal health insurance plan two years ago.

“Corporate insurance is enough,” he had said.

The Truth Corporate Employees Don’t Want to Face

Corporate health insurance is:

Employer-controlled

Limited in coverage

Full of sub-limits

Not designed for long hospitalizations

Taken away the day you resign or retire

And most importantly:

It has not kept pace with medical inflation.

Medical costs in India have increased 2–3x in the last 5–7 years.

Corporate policies haven’t.

MoneyNivesh Academy Takeaway

If you are a corporate employee in India, remember this:

Corporate health insurance is a benefit, not a backup plan

A personal health insurance policy is non-negotiable

Medical emergencies don’t ask:

Where you work

How much you earn

Or how confident you feel

They only ask one thing:

Are you financially prepared?

Amit learned this lesson the hard way.

You don’t have to.

Action Step (Do This Today)

Buy a separate family floater health insurance

Minimum cover: ₹10–15 lakhs

No room rent limit

Lifetime renewability

Buy it while you are healthy

Because one hospital bill should not be enough to erase years of hard work.

Calculate your ideal life insurance cover in under 2 minutes.